In Part 1 o f this series, we talked about how the FAFSA process can (and usually does) cause parents and students to overpay for college. The result of FAFSA is the family’s EFC – or Expected Family Contribution – the baseline amount you’ll pay for college. And what may seem like smart financial planning in the rest of your life, will often penalize you when it comes to college planning, resulting in a larger than necessary EFC.

f this series, we talked about how the FAFSA process can (and usually does) cause parents and students to overpay for college. The result of FAFSA is the family’s EFC – or Expected Family Contribution – the baseline amount you’ll pay for college. And what may seem like smart financial planning in the rest of your life, will often penalize you when it comes to college planning, resulting in a larger than necessary EFC.

But the EFC is just the starting point. The College’s sticker price minus the EFC equals the family’s Remaining Need (RN). So if a college costs $25,000 a year, the family with a zero EFC still still has a remaining need of $25,000 a year; while the family with a $10,000 EFC will need to come up with another $15,000 a year.

Where will that come from?

Thankfully, most colleges have gifting policies that will make up much (sometimes all) of the difference. While it’s nearly impossible for you to find on your own, a good college planner (like those I’m happy to refer you to) will know the gifting policies of every school in the country. You may discover that College A provides 100% of the remaining need; while College B provides only 60%. .

But that’s just part of the story.

‘Gifting’ is made up of two components. Outright gifting is a dollar-for-dollar reduction in the sticker price. The other part is student and/or parent loans the school will make available to you. Obviously free money is better than money that must be repaid. So College B – who makes up only 70% of the RN, but with all free money, may be better than College A, who makes up 100% of the RN; but only 50% is free money while the remaining 50% is parent loans.

Unbelievable Sidebar Factoid: Students used to be able to rack up nearly unlimited amounts of debt through student loans. Today, that is capped at $27,000 for undergrads. To make up the difference, a new category of ‘Parent Loans’ has evolved. But it turns out that parent debt is even more devastating than student debt. Today, there are a staggering 2,000,000 parents collecting Social Security Benefits while they’re still paying on parent loans (some are drawing Social Security just to pay on those loans), and a mind-boggling 300,000 of them are having their Social Security benefits garnished to pay their parent debt down!

What you’ll discover is that more expensive private colleges and universities often have significantly more generous gifting policies than state or community colleges and universities. Knowing this may land Junior at an Ivy League School instead of State U.

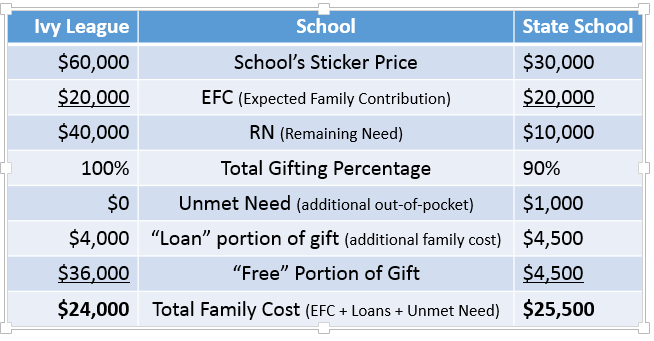

Here’s how it all works:

One more important footnote. Your EFC is not your EFC per child, it’s your EFC per family. Therefore if you have two or more kids attending college in overlapping years, the EFC is divided between the two. That means the remaining need is higher for each – which also means a school with a high gifting percentage (in this example, the private school) becomes even more important to your overall cost. In this example, two kids in the State School would cost $21,000 each; while two kids in the private, Ivy League School would cost $15,000 each.

Voila! An Ivy League School with a sticker price that’s twice your local state or community college, can actually be cheaper to attend. And this is not an isolated example. The simple fact is, private schools generally have larger endowments. Schools are required to distribute from their endowments each year. So – since private schools generally have a smaller student population and are better endowed, their gifting policies are typically much more generous than that less expensive state school.

Since we all want our kids to go to the best school they qualify for – at the lowest financial impact on the family, this is critical information to know. But it’s not on the School’s website. I can refer you to college planners that have a complete database of all colleges and their gifting policies. Simply ping me, and I’ll gladly hook you up.

Between optimizing your EFC, and leveraging the most generous schools gifting policies, hopefully college is looking a little more accessible and a little less frightening than it was – and there’s one more part to come, so stay tuned for Part 3 in this series.