It’s ‘back-to-school’ time – and even younger parents are thinking about how they’ll ever be able to pay for Junior’s college.

It’s ‘back-to-school’ time – and even younger parents are thinking about how they’ll ever be able to pay for Junior’s college.

Since many of our parents were able to pay for college – we naturally consider it a parental responsibility to do the same in return. The problem is that frankly, college wasn’t all that expensive a generation ago. Today – it’s outrageous – so paying for it means being much smarter and more informed about the options.

No parent wants their child to graduate with what is now $33,000 in student loan debt. You don’t have to be a college graduate to realize that starting life with that kind of debt load means delaying a home purchase, marriage, doing without, and then doubling down on retirement savings in the later years because all the money was used for debt payments in the earlier years.

One obvious answer is the tried and true 529 college plan offered by your state. These plans grow tax-deferred growth – and can be taken out tax-free as long as withdrawals are for college expenses.

But they have their drawbacks too. They can be fee-intensive, money taken out for non-college expenses is fully taxable and may be subject to penalty, investment choices are limited, most of your money is “at-risk,” and 100% of the money in these plans is counted against you and Junior when it comes to qualifying for most forms of financial aid.

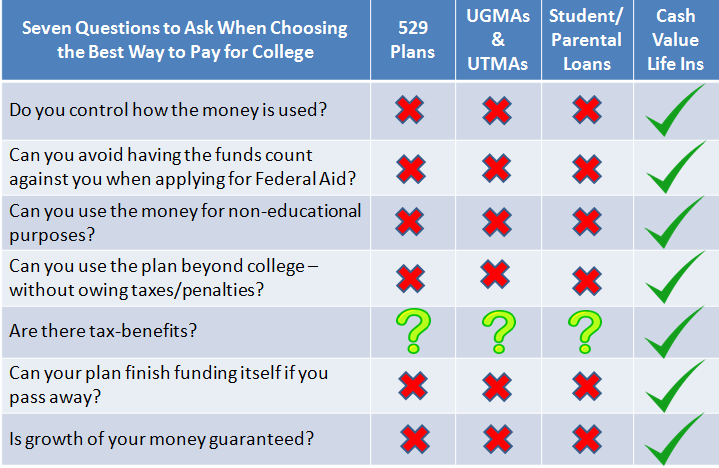

This cha rt compares some of the alternatives based on 7 questions to consider in evaluating alternatives.

rt compares some of the alternatives based on 7 questions to consider in evaluating alternatives.

While from time to time I extol the virtues of properly structured cash value life insurance, here’s one situation in which it can blow away the competition among college saving options.

In fact, the benefits and strategies of life insurance as a college planning vehicle are too numerous to cover here – but believe me – if you find a qualified life insurance agent who specializes in college planning strategies, it will be well worth your time.

So in addition to new shoes – a cool outfit – and notebooks, paper and crayons; consider your options carefully – plan – commit – and make Junior’s pathway one that doesn’t cramp your financial style – or theirs.