Ever meet an investment advisor who doesn’t wear a nice suit, drive an expensive car, or live in a posh neighborhood? Ever see an investment firm in a rundown strip mall, next to a Dollar Tree or Goodwill store?

There’s a reason. Accessing Wall Steet exchanges and Wall Street advice is expensive! How expensive? Experts think it’s between 3% – 4% of our annual account balance. The problem is – most average investors argue that point. In fact, Forbes says 95% of 401k investors insisting they pay no fees at all (they do).

Even those moving toward low-cost EFTs and ‘robo’ accounts (which dispense with human advice) are paying more fees than meet the eyes. Just go back to paragraph 1 and ask yourself this; ‘if I’m paying little to nothing, how are those guys buying those tailored suits, expensive cars, and nice homes?’

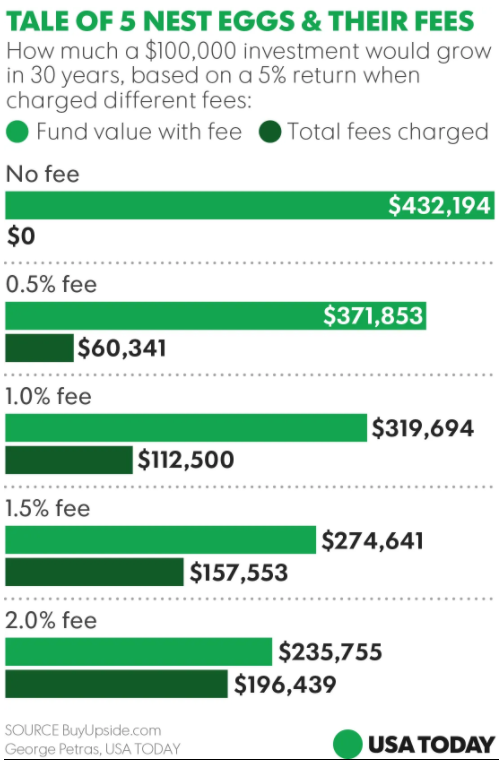

Regardless, investing fees and commissions have a much more dramatic impact on our investing outcome than we allow ourselves to believe. So rather than debate the ‘how much’ question, let’s just focus on impact. Here’s how USA Today characterizes it:

But even this doesn’t tell the whole picture. Why? Because first, nobody invests $100,000 one-time in their 30s or 40s – and lets it sit for 30 years? Second, those fees don’t go away after 30 years – they continue for life – and perhaps even beyond!

So we decided to build a model that represents a more typical investor. We compared two different strategies – a typical Wall Street investment account – and Life Insurance (yes – life insurance can be a great way to build wealth). We chose life insurance because the cost structure is inverse to Wall Street’s cost structure.

With a few exceptions, Wall Street fees are usually assessed as a percentage of a portfolio’s value on an annual basis. That means that as the account grows (which we hope it does), the fees grow with it. In an insurance policy built for wealth accumulation, the fees start out higher, but fade away over time – until in some cases – they disappear altogether.

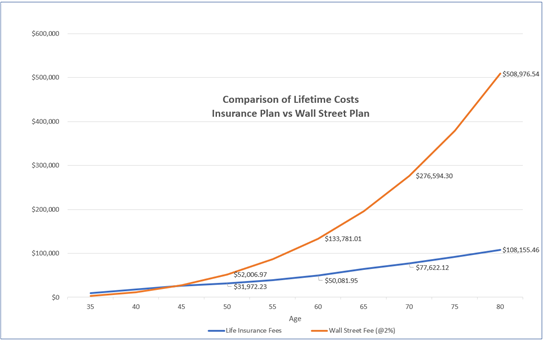

The exercise was designed to see which model had the greatest impact on an investor’s outcome – all other factors (growth rate, time, and taxation) being equal. The results were quite surprising. The table below shows the cost – through age 80 (roughly life expectancy) of a Wall Street Account (gold line) charging fees at a rate of 2% (well below expert projections), to a popular life insurance platform (the blue line).

The difference is staggering. The lifetime cost of the 2% Wall Street plan would be $509,000, while the same amount put into a life insurance platform – growing at the same rate – over the same period of time, would charge fees of just $108,000. That’s a $400,000 lifetime difference – and $400,000 buys a lot of lifestyle.

What’s more, the life insurance plan has a $900,000 tax-free death benefit at age 80 – meaning it will ‘refund’ 8X the amount of lifetime fees paid to own it.

So why don’t more people choose this option?

For starters, most don’t even know it’s an option, and Wall Street, who thrives on fee income, doesn’t push the strategy for obvious reasons. Others are dissuaded by the fact that in the first 15-or-so years (as can be seen on the graph), the insurance plan has higher costs than the Wall Street plan. And while it might seem short-sighted to look at the 15-year cost versus the 50-year cost – guess what – investors tend to be… short-sighted.

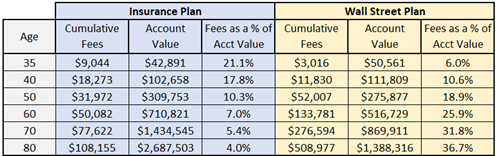

We can see this more directly in the table below, where the accumulated value of the Wall Street account exceeds that of the insurance account over the first several years. The cost of the insurance plan is much higher, and as a result, the account value is much lower.

Both plans show the outcome for a 30-year-old putting $750/month into the respective plans through age 66, growing their money grew at 6.03% annually. Fee are calculated in the Wall Street account at 2% annually, the life insurance fees are directly from the insurance carrier for this exact plan.

But that all changes somewhere around year 15, when the insurance plan yields a better outcome due to its diminishing cost structure, and that gap only widens over time. Perhaps even more revealing is that when the cost is viewed as a percentage of the accumulated cash in the respective plans, the insurance plan costs go down precipitously over time, and the Wall Street account cost just keeps getting larger and larger. In fact, both accounts received $324,000 of lifetime deposits ($750/month X 36 years X 12 months). That means the Wall Street advisor will take out more in fees than the investor put in.

The point isn’t to promote life insurance, it’s to demonstrate that smart investing decisions aren’t just a matter of disciplined saving, investing prowess, and return on investment. Often overlooked factors like fees, commissions, and other costs can make a bigger impact on our results than the things that outwardly appear to be more important.

In the world of magic (illusion), it’s called deception, ‘look over here, not over there.’ Those with discerning eyes have a much better chance of understanding the trick, than those that are mystified by the illusion. Pay attention to details like cost – and win the game.