It would be nearly impossible to function in today’s world without using a credit card from time to time. And so long as we pay the balance off each month – that convenience comes our way free of charge – and who doesn’t like free?

But carrying balances on our credit card accounts becomes perhaps the most expensive way of buying things imaginable. Why? Because credit cards don’t play by the same rules as conventional lenders.

In a typical loan transaction – say a car loan, a student loan, or a home mortgage – three elements go into an amortization calculation to determine the payment. If we were to borrow $5,000 at 18% for 5 years, an amortization calculation would require a monthly payment of $126.97.

Make that payment – on time – for 60 months – and we will have repaid the loan in full. We also know that our total of payments will be exactly $7,618.03, meaning we will have paid exactly $2,618.03 in interest.

Because we know all three variables – the principal amount ($5,000), the interest rate (18%), and the repayment term (5-years), the calculation works. It’s straightforward and logical. Both the borrower and the lender know exactly what the expectations are going in, so there’s no gray area – no opportunity for either side to say – down the road – ‘you never disclosed that.’ If the arrangement is unacceptable to either side based on an eye-wide-open analysis – the transaction doesn’t happen.

It would seem reasonable to assume that credit cards work much the same way – but they don’t. And because the rules under which they operate are opaque and give the banks an unfair advantage, they prey on borrowers and collect HUGE sums of interest.

Left in the dark however, cardholders will send the credit card bankers far more of our hard-earned money than necessary – to a point that seems borderline criminal. It’s not of course – but only because the credit card banks have strategically invested their influence in government regulators who write the rulebook in the banks’ favor – sanctioning the piracy in the process.

I want you to know exactly what’s going on – how it all happens – and how you can avoid it ravaging your finances.

How Credit Cards Set ‘Minimum Payments’

Rather than using the conventional method of determining a loan payment (the amortization calculation), credit card issuing banks use their own methodology – and you can be sure if favors them over you. There are two methods they may choose to employ:

Notice – there is no third element in the equation. Missing is the repayment term. That’s because they don’t want you to know how long it will take to repay their loan at the minimum payment – or how much interest you’ll pay if you do so.

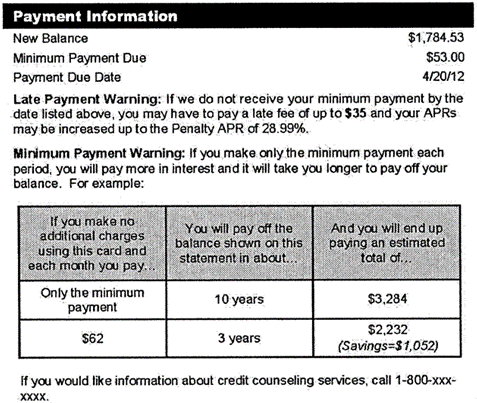

Actually, due to some consumer advocacy in recent years – you can know the answers to those questions. The answers are so bad that regulators now require repayment disclosure on your credit card statement – which most of us have never even noticed. Below is an example:

In this example, the minimum payment as calculated by the credit card company is just $53/month. But at that rate, it will take the borrower 10 years to repay the entire amount, and they’ll repaying nearly twice as much as they borrowed.

Now imagine the power of knowing that by over-paying the $52 minimum by just $9/month – and making $62 payments instead – you could save over $1,000 in interest. It’s knowing that kind of information and having the drive to act upon it that puts us in control. It’s our continued ignorance of these matters that are making the banks rich – at our expense.

What I’m about to show you should shock you. A few notes about the figures that follow.

- First, we are assuming there are no new charges, late fees, or other charges – all we’re doing is making minimum payments against a static beginning balance of $5,000.

- Second, I’m assuming that the calculated minimum payment is subject to a minimum of $25.00 – which is pretty standard among credit card issuers.

- Finally – I’m using an 18% rate of interest – again – fairly standard in today’s environment.

Here we go:

There are several takeaways from this analysis that are important for you to understand:

- First – the credit card companies quoting an interest rate of 18% is a complete joke. It is financial sleight-of-hand. We know what 18% interest looks like – and it doesn’t look like this. Only in the underground world of mathematical trickery could a bank collect the kind of money you see above – and call it an 18% rate of interest.

- Remember that had we borrowed the same $5,000 at the same interest rate (18%), repayable over 5 years using an amortized payment calculation instead of a crazy credit card calculation, our payment would be only slightly higher at $126.97; we’d repay 100% of the debt in 60 months; and our total interest cost would have been $2,618.03. Look at the difference.

- An obvious takeaway is NEVER, EVER, UNDER ANY CIRCUMSTANCES – treat a credit card loan like a conventional loan – and repay it making only minimum payments.

- If we were smart enough to pay $126.97 a month (as in an amortizing loan) instead of the alluringly deceitful minimum payment calculated by the credit card bank – the credit card loan will perform exactly like the amortizing loan. We’d be fully repaid in 60 months at a total interest cost of $2,618.03.

- Even if cash was tight – and it wasn’t possible to keep up a routine of $126.97 monthly payments, but you could somehow find a way to pay an extra $20/month, the repayment time (Method 2) would come all the way down from 169 months (14 years, one month) to 100 months (8 years, 4 months) – and the total interest cost would fall from $5,643 to $3,491.

Managing and extinguishing debt is much more a function of knowledge than it is financial resources. Albert Einstein once said those who understand compound interest earn it – those who don’t pay it. You can see in the discussion we’ve laid out just how true that is.

Become a student of your own debt – learn the mechanics of interest and payments, and debt – and take control of your financial future forever. Of course if you ever need help – we’re here for you.