Shortly after the pandemic began, the Trump administration suspended payment requirements on government student loans. The Biden administration recently extended payment deferment through September 2021. Deferment – in this case – means that not only is the required payment suspended, so is the calculation of interest.

If your financial situation is such that you need to take advantage of the deferment period to get other financial priorities under control – the relief is certainly welcome. But for those who are able to make payments – a very interesting opportunity has revealed itself.

Under a normal payment scenario, part of each payment reduces the principal balance owed, and the remainder of the payment goes to interest. The proportion of each is determined through an Amortization calculation – a formula banks and lenders use to determine payments on loans and the rate at which they collect interest.

Among other things, amortization allows the interest calculation to be ‘front-end-loaded’ – meaning a greater proportion of the early payments go to interest, and a greater portion of the later payments go to the reduction of principal.

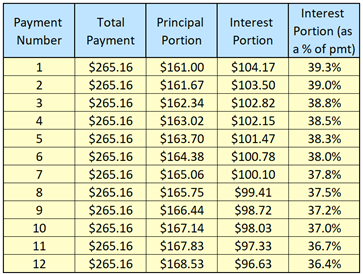

Below is a breakdown of the first 12 payments on a $25,000 student loan, repayable over 10 years at an interest rate of 5%. The required monthly payment is $265.16. In the first month, nearly 40% of that payment goes to interest. That proportion is reduced as time goes by, but it is substantial, nonetheless.

The significance of that figure is that each dollar paid is only about 62% efficient in terms of it’s principal-reducing impact.

But during the deferral period, if you are able to continue making payments – in this case $265.16/month – 100% of the payment goes to the reduction of principal. Your dollars are 100% efficient in reducing the principal balance on your loan.

In this simple one-year snapshot, continuing those payment – even though not required – would reduce the principal balance by an additional $1,200 – nearly 5% of the total principal balance. That’s a pretty huge reduction in principle – and if you were making the payments anyway – it cost you NOTHING.

When I share this good news, the question always comes up, “I don’t want to make payments if there’s a possibility my loans will be forgiven.”

Okay – that’s not really a plan, and arguably, its not a responsible point of view (you did borrow – you did learn – you do owe the money), but I get it.

Here’s a twist on the idea that acknowledges that possibility. Open up an interest bearing savings, checking, or money-market account at your local bank – and keep making payments to that account as you would on your student loans.

- If the deferral period is extended – you’ll be banking 100% principal-efficient dollars for the day the deferral period ends,

- If loans are forgiven altogether – you have a nice chunk of savings that can be used for another purpose,

- If loans are partially forgiven you still have a huge head-start on the remaining balance, and

- If payments resume with no forgiveness – send the savings in that account in – knowing that you’ve used the deferral period to take a nice bite out of the remaining balance that cost nothing.

Seldom does the government give gifts. This is one – only if you can see it as a gift, and understand how to leverage it to your advantage.