Over the past 5 years, I’ve informally polled audiences on their opinion of future tax rates. “Do you think tax rates when you retire will be higher or lower than they are today?”

Over the past 5 years, I’ve informally polled audiences on their opinion of future tax rates. “Do you think tax rates when you retire will be higher or lower than they are today?”

Everyone thinks future tax rates will be higher. We’re resolved to the reality that $17 trillion in debt will – sooner or later – necessitate higher tax rates.

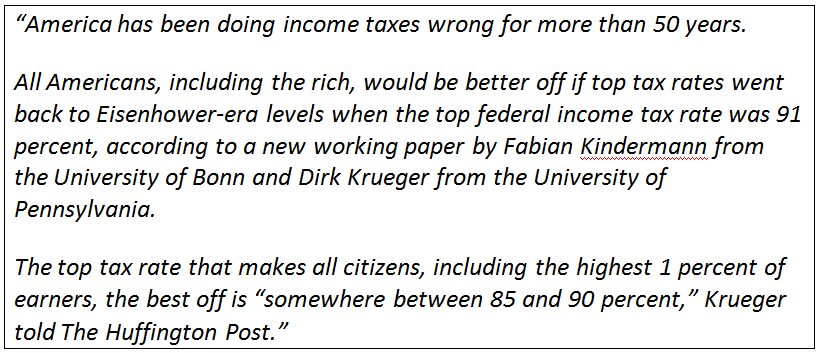

But the bad news is that ‘sooner’ may almost be here. A recent article in the Huffington Post starts out this way:

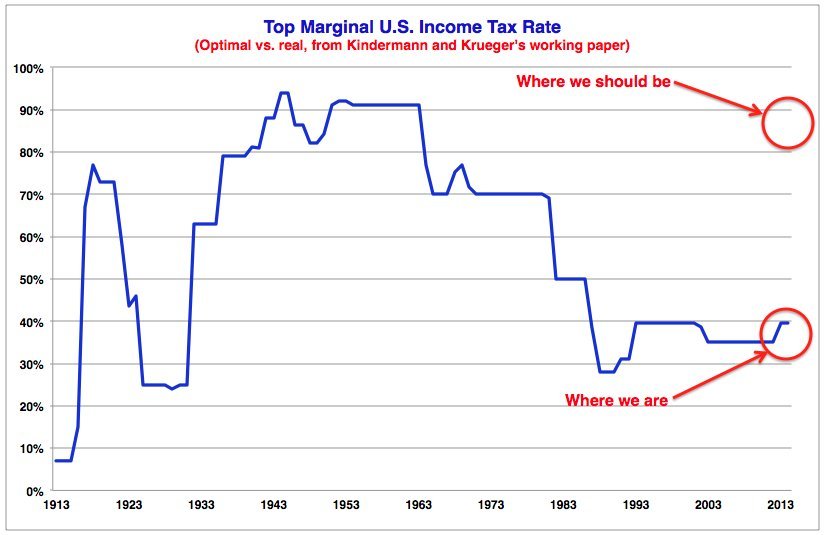

For perspective, the article then offers the following chart, showing historical top marginal tax rates.

Look at how much taxes have gone up over the last few years with little fanfare, media coverage, or debate.

Most of us aspire to retire someday. We won’t be earning money from work – but living on the nest-egg we’ve accumulated and the earnings on that nest egg.

So what do you do if tax rates go up? If you’re close to – or in retirement – there are few – if any – strategies that can ameliorate the impact of taxes.

So what gives? Lifestyle. Ma and Pa are just going to have to make a few less trips to the cafeteria. But that’s not what retirement is supposed to be about – figuring ways to do with less because the government decides to confiscate more.

All this emphasizes the importance of tax planning at an early age. It means tax-deferred plans – IRAs, 401ks, and others – even with their ‘matching funds’ – are turning into long-term tax-traps that MUST be avoided.

Savers and investors should turn their focus to tax-free income sources – the kind that makes it completely irrelevant what happens to future tax rates.

Wall Street doesn’t do ‘tax-free’ very well. So if you want to become educated and enlightened on what is out there that is truly tax-free – you have to search it out. Or – just keep crossing your fingers and hoping folks like Kindermann and Krueger don’t get much traction.