Our pre-retirement inattention to Medicare has left it a playground for politicians – and they’ve been having fun crafting surprises that lie in wait for you.

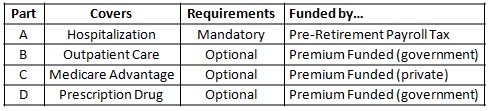

There are four parts to Medicare (health insurance for retirees):

We’ll skip comment on Parts A and C in this writing, and focus instead on Parts B and D.

Premiums for these programs are determined by government “means” testing (those who make more – pay more) – and those premiums are automatically deducted from your Social Security benefit (like a payroll tax).

And means-testing is the real gotcha!

“Means” are determined by MAGI – Modified Adjusted Gross Income. MAGI is defined as:

Ordinary Adjusted Gross Income (from your tax return)

+ Tax Exempt Bond Interest (and you thought it was really tax-free)

+ Wages and Tips

+ Capital Gains (so much for those low Capital Gains Rates)

+ Social Security Income (woops – I thought those were untaxed too)

+ Dividend Income

+ Qualified Plan Withdrawals (401k, 403b, IRA, etc.)

+ Gain on the sale of a home (over a certain threshold)

+ Most Annuity Income

Once MAGI exceeds the government determined threshold (currently, $85,000 and $160,000 for individuals and couples respectively), Parts B and D premiums increase dramatically.

And not only were premiums adjusted upward as recently as 2012, there is pending legislative action that would increase premiums again and lower the thresholds to $65,000/$130,000 respectively. Ouch – can someone call a doctor?

This places renewed importance on income structuring – arranging your affairs in a way that shifts income from categories that count toward the MAGI calculation – to those that don’t – and unfortunately – that list is pretty short: distributions from Roth IRAs, Reverse Mortgages, HSAs, and loans from cash value life insurance.

Of those, the one that is virtually unlimited – in terms of how much you can put in – how much you can take out – and how protected your money is while in the plan – is cash value life insurance.

That same income is completely tax-free, and many of todays cash value life insurance plans allow additional withdrawals against the insurance benefit for long-term-care and related needs in certain circumstances.

If you don’t have a trusted retirement planning professional, you need one. He or she will likely be different than your broker, financial advisor, CPA, or estate attorney. And you need them NOW – regardless of your age – while there is still time to plan.