Most people don’t even know that today’s cash-value life insurance products are a great way to build wealth when properly structured.

But even if you were open minded to the idea that it might be worth looking at – most would surely assume that because life insurance includes a death benefit – it must be a much more costly way to build wealth than other alternatives. Certainly the nay-sayers beat that drum.

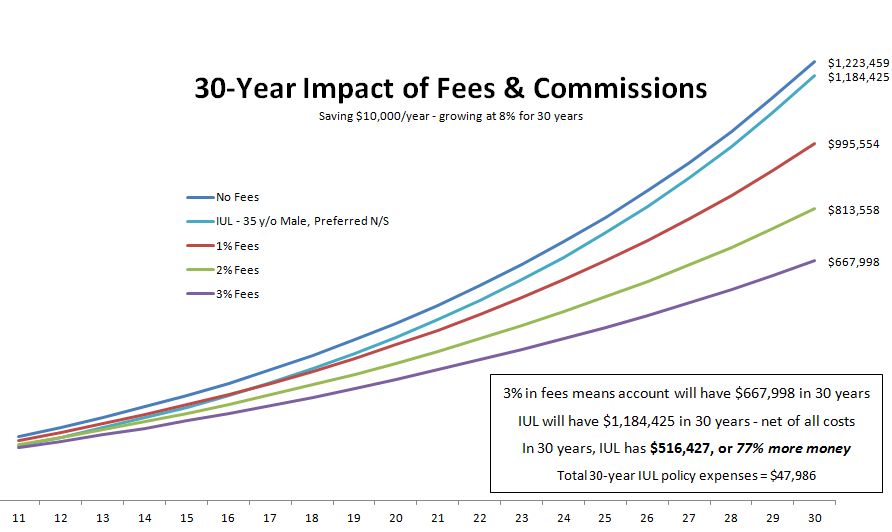

But the truth is – when properly structured, cash value life insurance can be perhaps the least costly way to build wealth and retirement income. Here’s a chart that makes the point:

The chart shows the impact of fees on a typical investment account over 30 years. The top line is the “no fee” benchmark of an account into which a 35 year-old deposits $10,000 a year, and grows their money at 8% annually. Our investor would end up with a cash balance of $1,223,459 if there were no fee impact at all.

The chart shows the impact of fees on a typical investment account over 30 years. The top line is the “no fee” benchmark of an account into which a 35 year-old deposits $10,000 a year, and grows their money at 8% annually. Our investor would end up with a cash balance of $1,223,459 if there were no fee impact at all.

But any strategy will have some fee impact. So the other lines show the impact of putting the same money into a properly structured life insurance plan – and growing it at the same rate – over the same period of time. Total cost: $47,986 – leaving a balance of $1,184,425.

Now look what happens when we pay Wall Street fees of 1%, 2%, or 3%. Most experts think most of us pay about 3% in total fees, costs, and commissions each year (although most investors will argue the point). If they’re right – the insurance plan will have more than a half a million more dollars than the Wall Street plan.

But even at just 1% in fees – the insurance plan beats a 12% Wall Street plan by almost $200,000 – and for most – that’s real money!

Cash value life insurance offers a number of other advantages – no risk of loss to market fluctuations, no taxes on distributions, living benefits in the event of long term disability, and of course – it’s tax-free death benefit.

It might be worth taking a new look at an old product.